{kind=link}

I’m assuming you already know you want to buy a life insurance policy to provide financial protection for your family and loved ones. But before you do, your first step is to figure out how much life insurance you actually need. This is as important as, if not more than, choosing the right type of life insurance policy. But the process can be a little time consuming and somewhat overwhelming with tons of questions. Stick with it. It’s worth it. The end result can be rewarding! And you will have done your personal financial check-up at the same time.

Finding the Right Online Calculators

Figuring out your insurance needs can be tricky. I have tried a dozen online life insurance calculators. They all act like some sort of “black box.” A magic number pops out from the box after you input a quantity of personal financial information. I hate to say but I don’t like most of them, especially some of the well-established online insurance quote services. Their websites have such an outdated, old school interface; it just ruins my experience. I feel like I’m going back to the Dark Ages.

I hate to sound too harsh but I am a consumer who loves new technology. I am a fan of Apple and new services like Uber. These companies consistently support a seamless online experience and offer personalized customer service. For the most part, the insurance quote engines do not.

I also found some calculators were either too simplistic or too complicated – to the point that I couldn’t figure out what I was supposed to put in. However, from among all the ones I tried, I did like the calculator from Policy Genius and the one on the Life Happens site. They provided an intuitive interface and asked me the right amount of information to make me feel that I was truly getting a personalized quote. They both can display an itemized list where you can track how your insurance needs numbers add up. I also liked the message from Policy Genius: “No pushy sales. Guaranteed.” This is exactly what I need as a modern consumer. And Life Happens is a non-profit organization. I like its mission to help Americans take personal financial responsibility.

There Is Also the DIY Method

It doesn’t take rocket science to come up with how much insurance you need without using a packaged insurance calculator. Everyone can do it with a little help. You just need to ask yourself a bunch of specific personal financial questions and then you only need to know some simple mathematical calculations. It can be easy to do it using a spreadsheet. When I shopped for my life insurance policy, I chose the DIY approach because I like to see how things are adding up and a spreadsheet lets me do this.

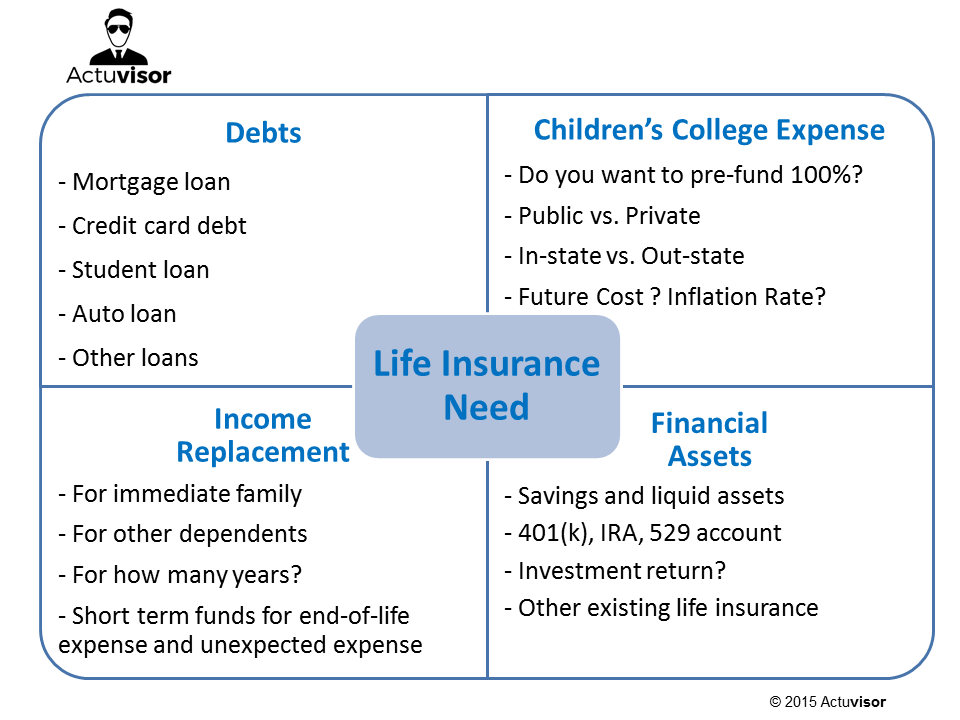

No matter which approach you take, these four (Debts, Income Replacement, Children’s College Fund and Financial Assets) building blocks are the fundamental pieces of information you need to know to determine your life insurance needs. Actuvisor has created a chart to help with this step.

No matter which approach you take, these four (Debts, Income Replacement, Children’s College Fund and Financial Assets) building blocks are the fundamental pieces of information you need to know to determine your life insurance needs. Actuvisor has created a chart to help with this step.

Now, My 7 Tips for Using Online Life Insurance Calculators

1. Build the Foundation

A good way to start is with the simplest case first and then build it up. I recommend you first build a scenario of your basic financial needs without children if you have them, and then add each child’s needs in one at a time. This way you can see how your insurance needs change based on each additional piece of information you add. You probably know by now I like transparency. I have built many financial models in my career and I always check the reasonability of each model. Most of these calculators don’t let you do that. Besides, I found that a few of the calculators tend to overstate your insurance needs. This is not too surprising since many of the online insurance agencies want to sell you more life insurance. I like to understand my true needs and not be oversold. By building the foundation myself, I have a much better idea of how accurate the results will be.

2. Check Out Two Life Insurance Calculators

It is always a good idea to check out at least two calculators before you make your decision. No two life insurance calculators are the same. They are all built with different assumptions and the results can vary significantly even for a simple case. I recommend that you print out the itemized lists and compare them side-by-side. The calculator is just a guide and you can always adjust the number up or down to fit your true needs.

3. Debts

Having a mortgage loan is one of the biggest reasons for people to buy life insurance. I bought mine for the same reason. I wanted my loved ones to live a debt-free life when I am no longer around. I recommend you factor in the full mortgage loan balance that you owe right now. The stress of a possible foreclosure can be devastating for many people. If something happens to you, you don’t want your family to have to go through that. Just ask the people who experienced this situation during the financial crisis in 2008. You also need to figure in any other major loan debts you may have, such as high credit card debt or outstanding student loans. It’s good to have a financial cushion for your family to be able to handle those as well should anything happen to you.

4. Income Replacement

To compute how much income your family would need, use these guidelines:

- Do you want your family to maintain the same standard of living? If the answer is yes, I recommend you use your current after-tax income.

- The income replacement period should account for at least 5 years. If you have a stay-at-home partner, you might want to go longer. Will your partner be able to resume full time work right away? If not, then you might want to figure on a longer income replacement period. If you have young children, you might also want to extend the number of years.

- If your life insurance will pay off the mortgage loan, you can subtract the mortgage payment.

- For some families, just paying off the mortgage and not having the mortgage payment is sufficient for the family to live on the surviving partner’s income.

5. Children’s College Expense

The first question you have to ask yourself: Do you want to pre-fund 100% of your children’s college expense?

- Both Policy Genius and Life Happens allow you to choose between public or private college and the price tags vary significantly. Policy Genius even allows you to choose between in-state and out-of-state. This is a nice feature for further breakdown, but this may not necessarily give you a more accurate outlook.

- The college expense component can vary drastically between calculators. For a 4-year private university/college, Policy Genius assumes the current cost of $232,350 compared to $169,676 for Life Happens (see footnote). You may want to check out the itemized list to better understand the numbers. I was curious and looked up the costs of five private universities from CollegeCalc.org. The college costs are closer to Policy Genius.

- What if you only want to pre-fund 50% of the college expense? Neither of the two calculators allows you to compute a portion of the college expense.

- The cost for someone who enters college today is significantly different than for someone who will enter in 18 year’s time. All calculators that I tested implicitly assumed an annual inflation rate in the model, ranging from 5% to 9% annually.

6. Financial Assets

Your financial assets can be used to offset the needs of life insurance. Some calculators build in a 5%-6% annual investment growth. We have seen that the values of some financial assets can be extremely volatile, both during the recession and even now with everything going on in the global markets. Since you can’t really predict the timing of your death (Yes, it is true even for an actuary!), I don’t mind being a little conservative and assuming no future investment growth. If the insurance calculator lets you, you can do this by simply taking it out to determine your insurance needs without investment growth.

7. Your Life Insurance Calculations Are Based on Your Life Today

All insurance calculators only tell you the insurance needs you have today, but your needs may decrease over time. Your children will enter and graduate from college. You will pay down your mortgage loan. You will save more in your retirement fund. In the next post, I will share how to customize your term life insurance to account for these changes and possibly save you hundreds or thousands of dollars.

An online insurance calculator is still a great approach if you use it mindfully. After you figure out your insurance needs, it’s time to look for the right life insurance product to fit your needs. I’ll write more about that later. Because whether you end up choosing term life insurance or permanent life insurance, knowing how much you actually need is always the first step.

Footnote: I input a scenario assuming an 18-year-old attending an in-state private college and looked up the insurance needs from the two calculators.

Disclaimer: This post is solely based my own experience and opinions. I have no affiliation with the companies mentioned in this post.